If you own real property in Colorado but your primary home is located outside the State of Colorado, you should be aware of a possible 2% withholding tax when you go to sell that Colorado property. Our colleagues at Land Title Guarantee Company have provided us with the following information to assist our sellers in fully understanding the costs associated with selling a Colorado property.

In general, sales of Colorado real property valued at more than $100,000 and made by non-residents of Colorado, are subject to a withholding tax in anticipation of any Colorado income tax that could be due on the gain of the sale.

Any sale that shows a non-Colorado address for the transferor may be subject to this withholding.

This law affects non-Colorado residents or those parties moving out-of-state and not purchasing another primary residence.

The amount, if withheld, shall be the lesser of 2% of the sales price of the property or the net proceeds.

However there are exceptions to this 2% withholding. Withholding shall not be made when:

- The selling price of the property is not more than $100,000;

- The transferor is an individual, estate, trust, or partner and both the Form 1099-S and the authorization for disbursement of funds show a Colorado address for the transferor;

- The transferee is a bank or corporate beneficiary under a mortgage or beneficiary under a deed of trust and the Colorado real property is acquired in judicial or nonjudicial foreclosure or by deed of lieu of foreclosure; or

- The transferor is a corporation incorporated under Colorado law or currently registered with the Secretary of State’s office as authorized to transact business in Colorado;

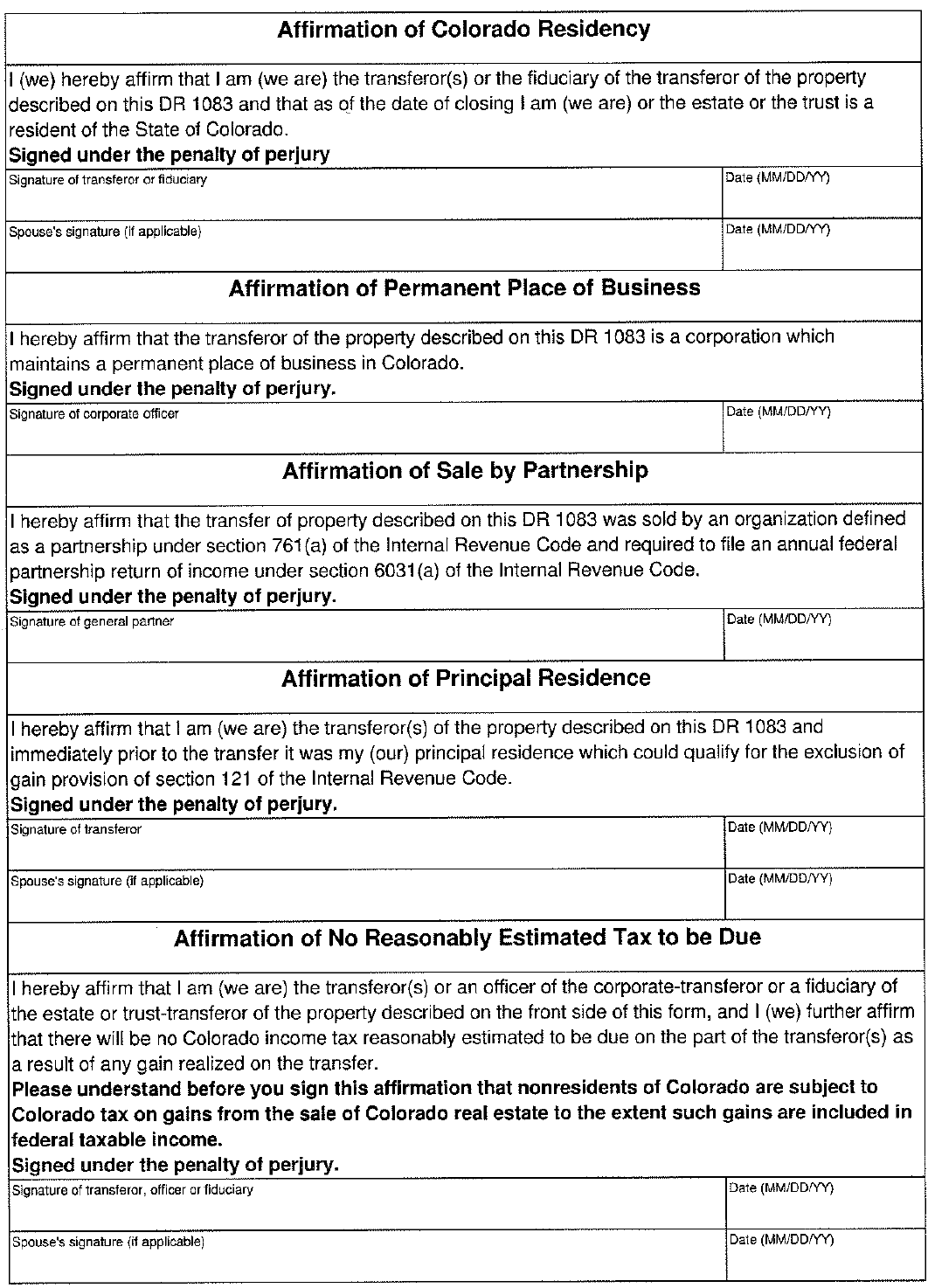

- The title insurance company or the person providing the closing and settlement services, in good faith, relies upon a written affirmation executed by the transferor, certifying under penalty of perjury one of the following:

- that the transferor, if an individual, estate, trust or partner is a resident of Colorado;

- that the transferor, if a corporation, has a permanent place of business in Colorado;

- that the Colorado real estate property being conveyed is the principal residence of the transferor which could qualify for the rollover of gain provisions of section 1034 of the internal revenue code;

- that the transferor, if a partnership files an annual federal partnership return of income under section 6031 (a) of the internal revenue code;

- that the transferor will not owe Colorado income tax reasonably estimated to be due from the inclusion of the actual gain required to be recognized on the transaction in the gross income of the transferor;

- no net proceeds, there is no corresponding paragraph to sign. The sellers settlement statement is sent out showing no proceeds to the seller.

If the out-of-state resident can agree to an affirmation, they should sign on that corresponding paragraph on page 2 of the form.

If this is a short sale or the seller is not receiving any proceeds, then a settlement statement will be attached on page 2 of the form.

If this is a short sale or the seller is not receiving any proceeds, then a settlement will be attached to the DR1083 to show “No Net Proceeds”.

By law, all completed forms are to be sent in to the Colorado Department of Revenue within 30 days of the closing date.

If you know you are an out-of-state seller, it is important to discuss this with both your Realtor and the closer working with the title company handling the closing. You should also consult your accountants if you have any questions as to the collection of the 2% withholding.

Below is Page 2 of the form this article discusses: